FE501 – 1012

FE501 – 1012Fund Allocation ProblemFunc Allocation - Matrix-Vector NotationStandard formSupplier-warehouse-user ProblemSolving with Excel Solver:Update: 2022-10-24TOYCO ModelAnswer ReportSensitivity ReportStandard form of LPSSurplus and Slack valueGraphical solution ProcedureExtrasStanford cvx

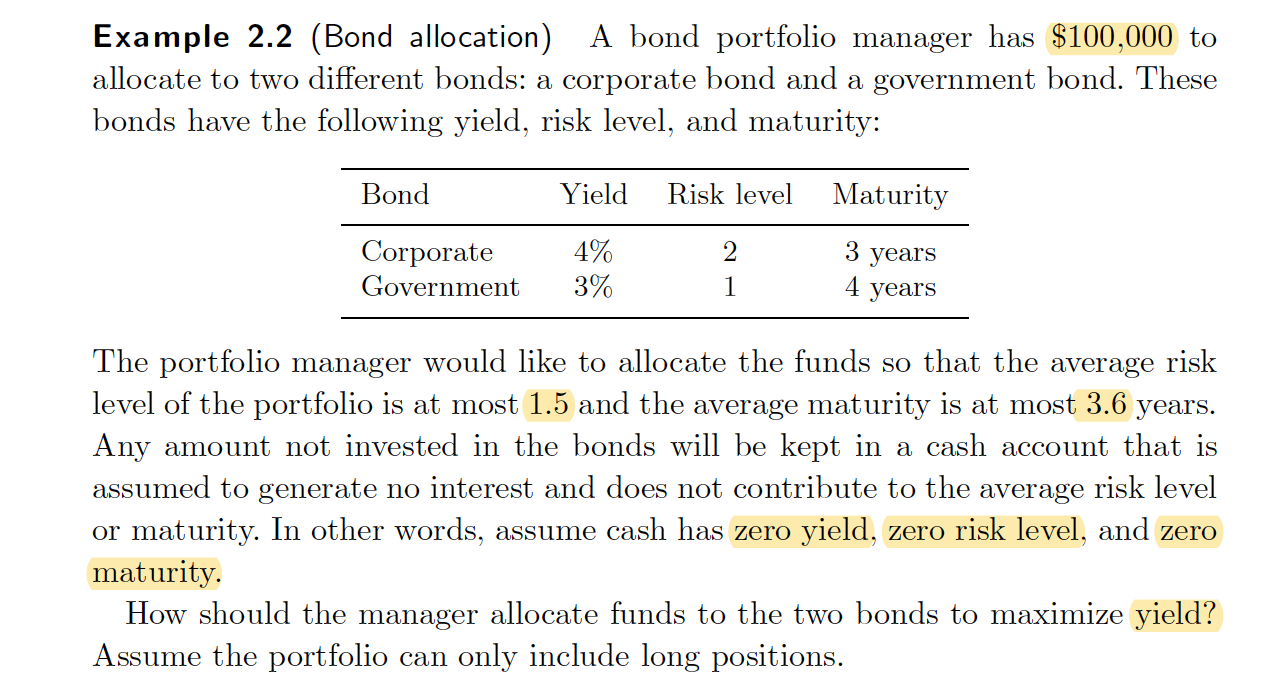

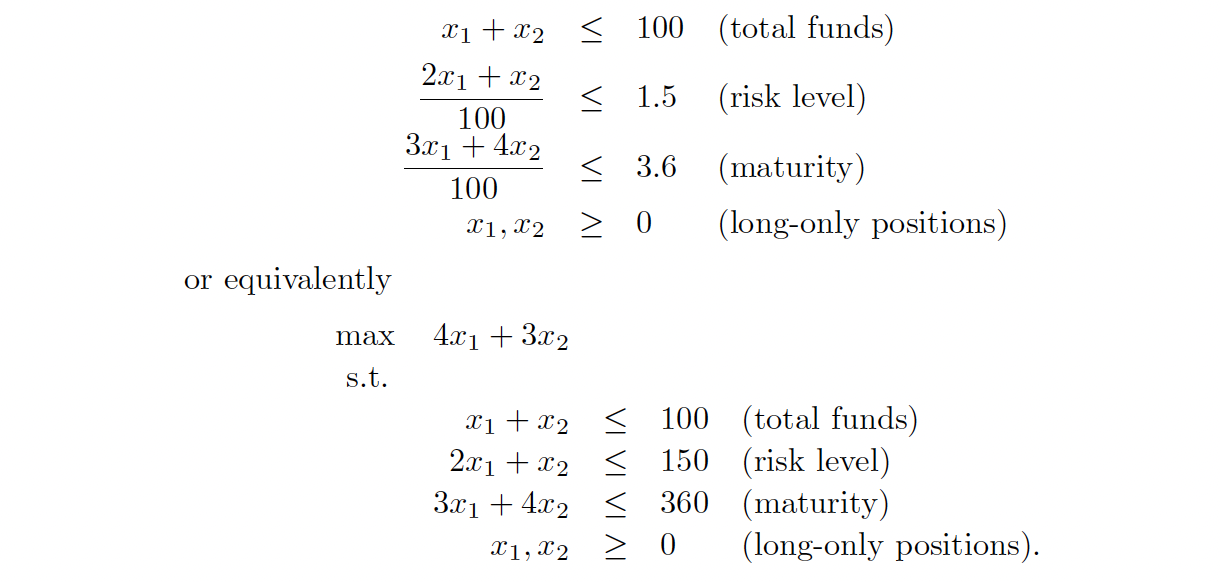

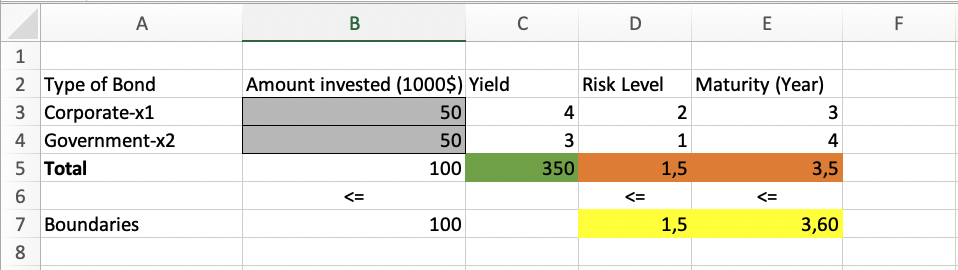

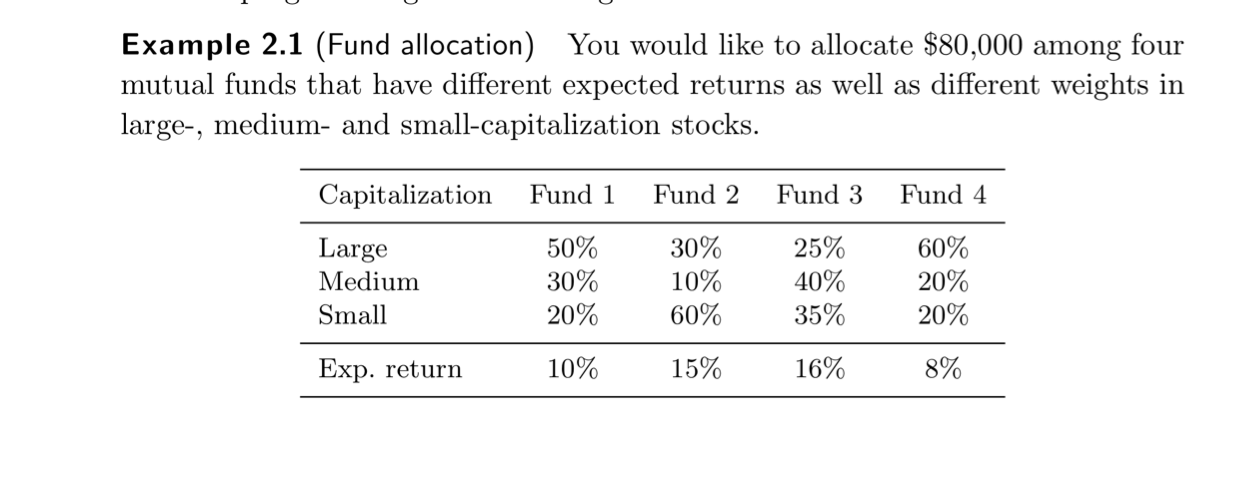

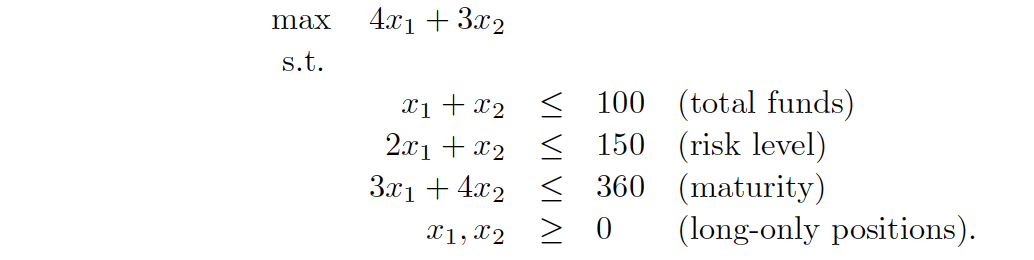

Fund Allocation Problem

Variables:

Objective:

Constraints:

Note on this problem:

Because they have different Risk Level and Maturity, when then original problem say avarage risk level or the avarage maturity it is not the arithmetic mean, this is here calcyulated as weighted arithmetic mean or weighted mean 1

here the weigheted avarage is calculated as:

Func Allocation - Matrix-Vector Notation

Standard form

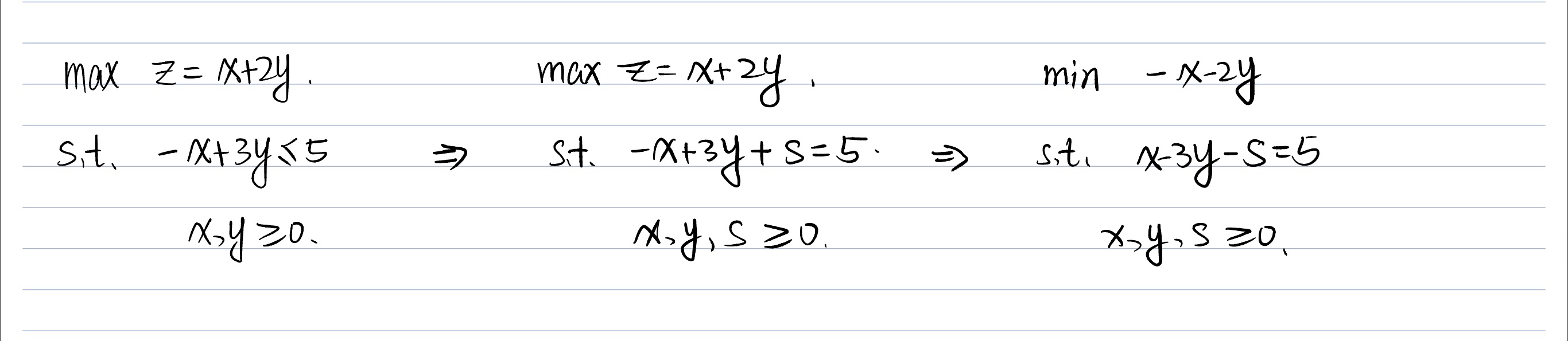

A linear programming model is in standard form if it is written as follows:

Any linear program can be rewritten in standard form. In particular , inequality constraints, can be rewritten as equality constraints after the introduction of a so-called slack or surplus variable.

For example ,

can be written as:

More generally, a linear program of the form

can be written as

It can be rewritten , using matrix notation, in the following standard form:

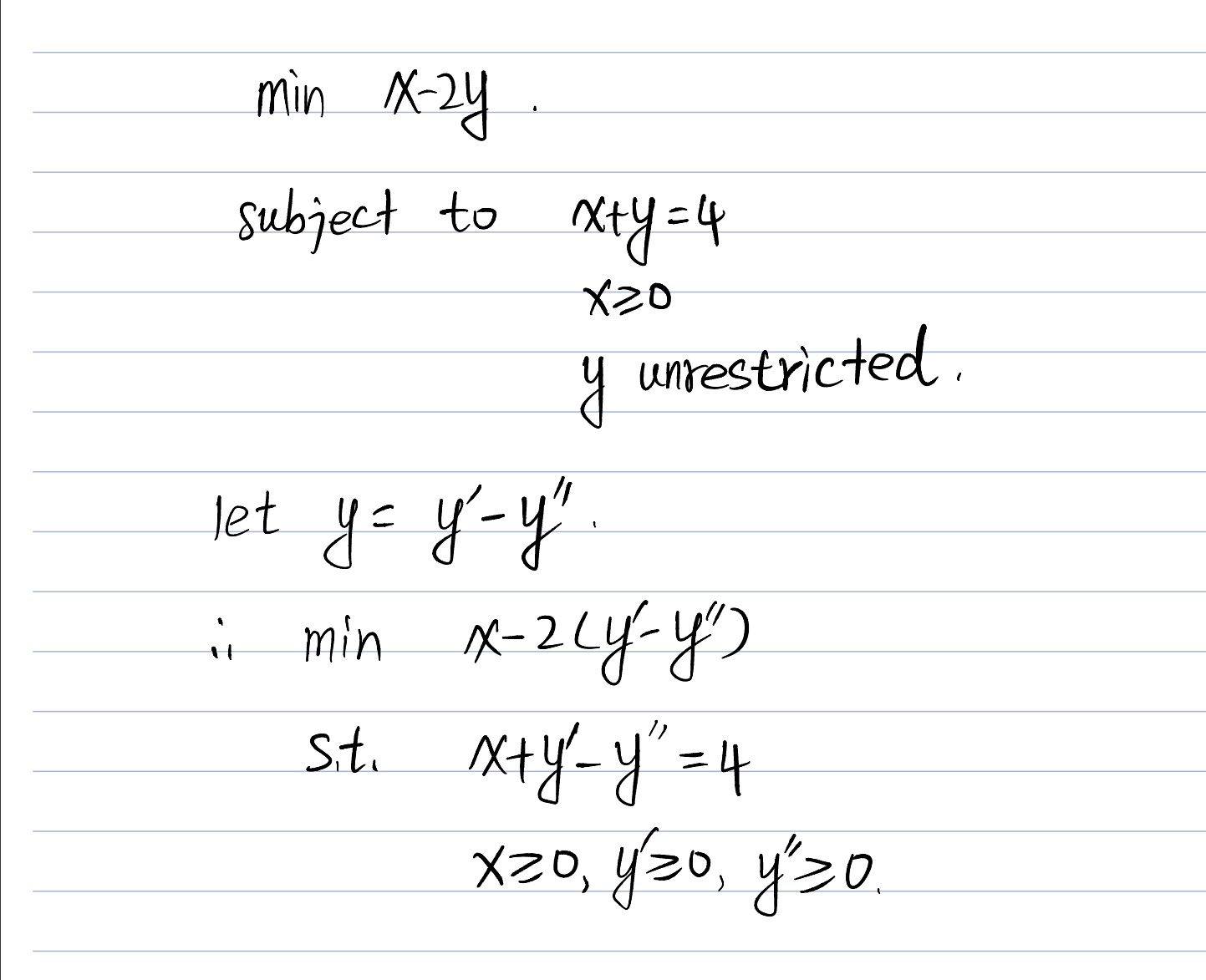

Un restricted variables can be expressed as the difference of two new non-negative variables. For example,

The unrestricted variable x can be replaced by

It can also be rewritten, after adding slack variables and using the matrix notation in the following standard form:

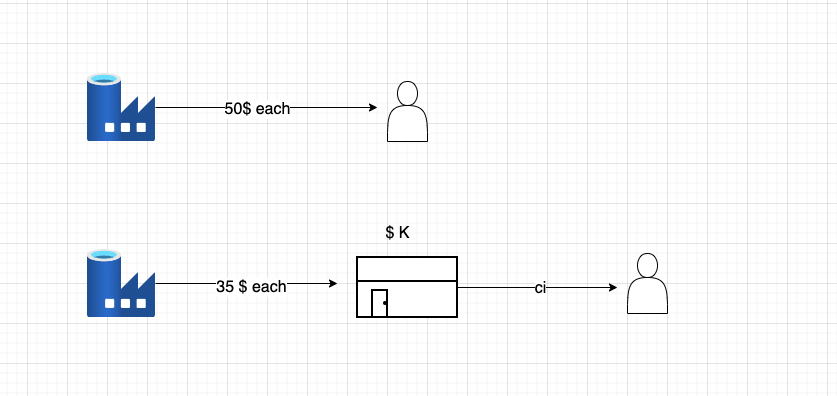

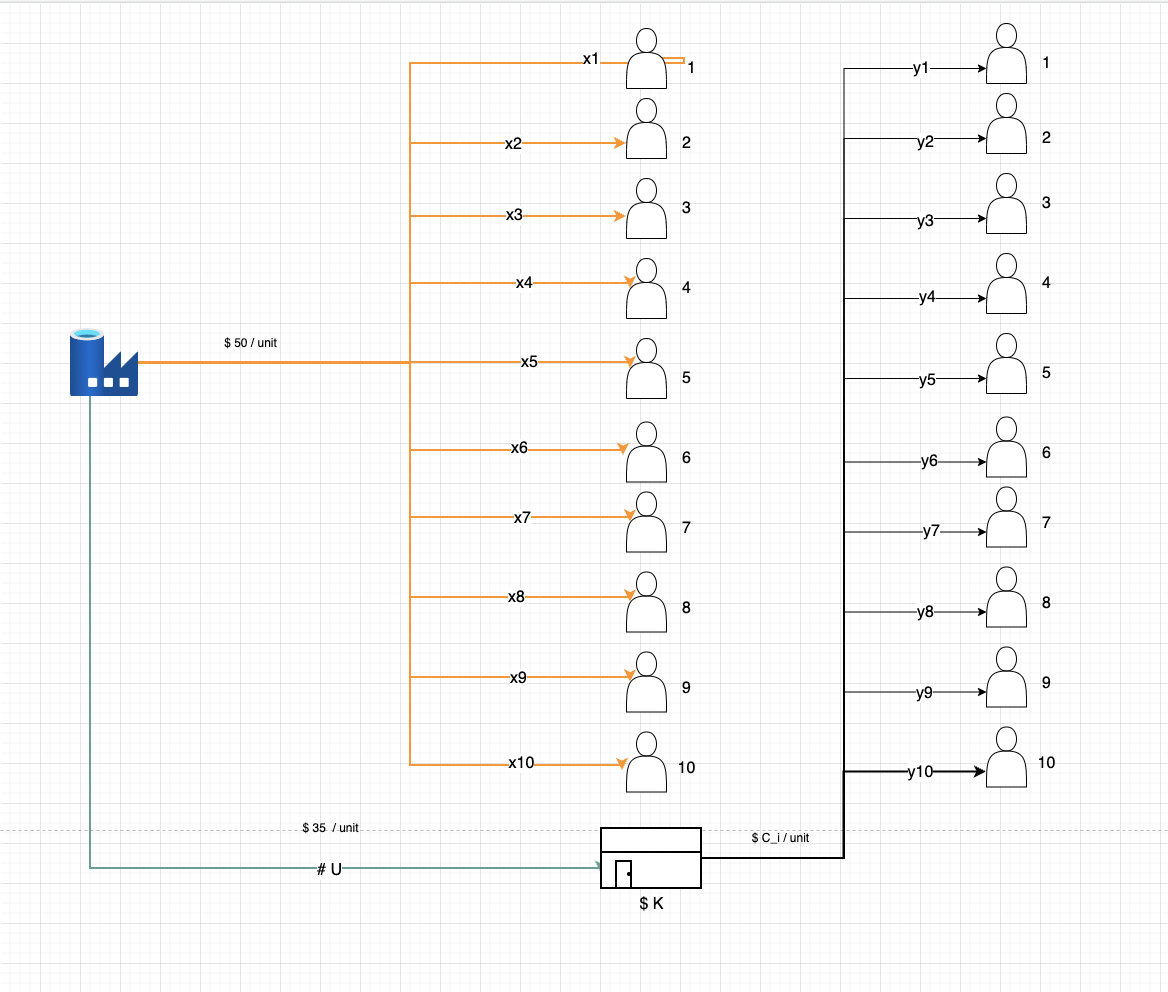

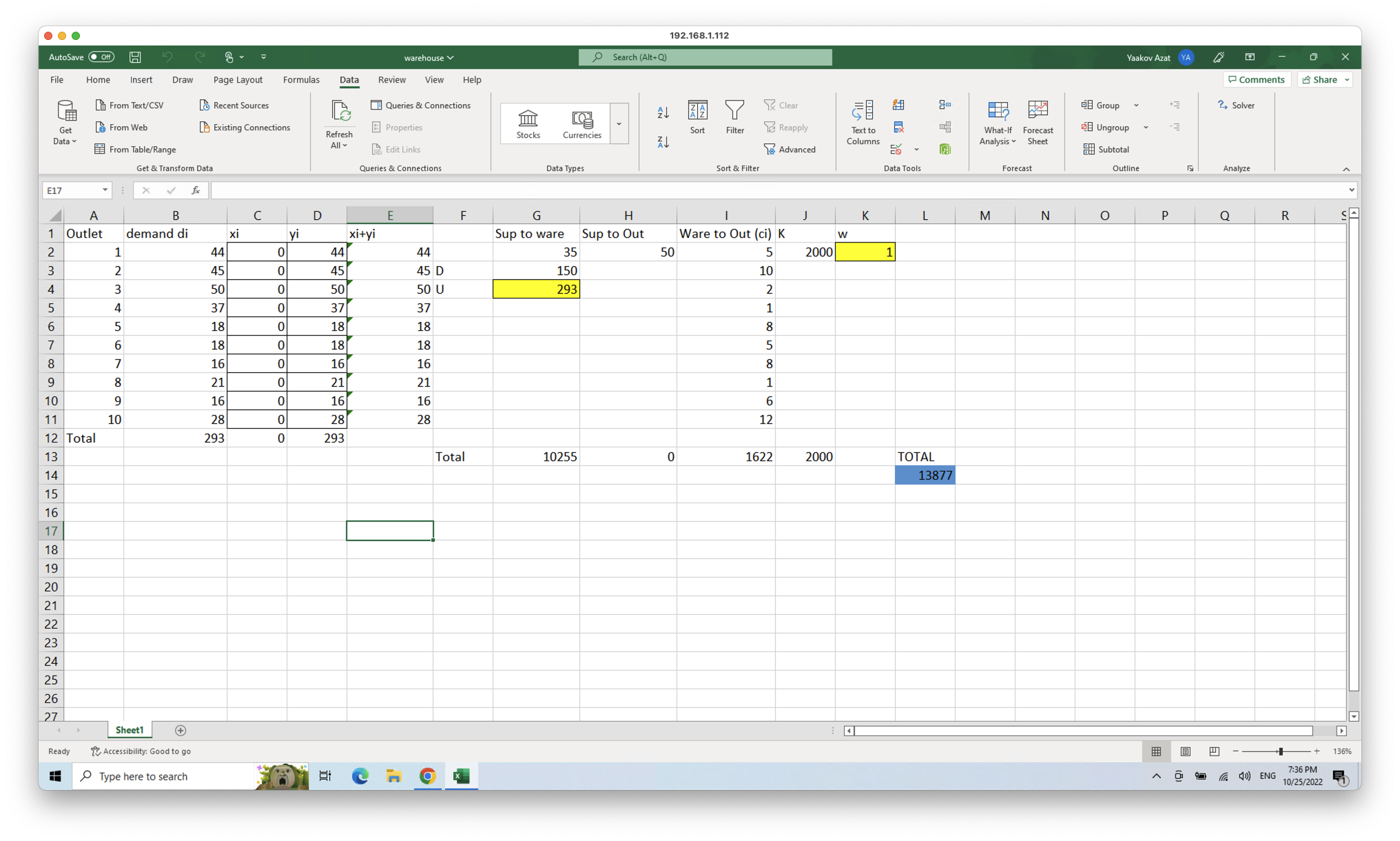

Supplier-warehouse-user Problem

Q: Suppoe we are retailer and we have 10 outlets as

Decision variables and their boundaries

D minimum required amount for delivering from supplier to warehouse. (

- Noticel: In the computation process, this become

- Noticel: In the computation process, this become

if we do not lease ware house (

if we lease ware house (

- U maximum should be smaller than sum of

- U minimum should be greater than sum of

- U maximum should be smaller than sum of

So if we combine (1) and (2) :

So if we combine (1) and (3) :

w =

Objective Function

Monimize overall cost, that is :

Cost from Supplier to Outlets =

Cost from Supplier to Warehouse =

Cost from warehouse to Outlets =

Cost of leasing warehouse =

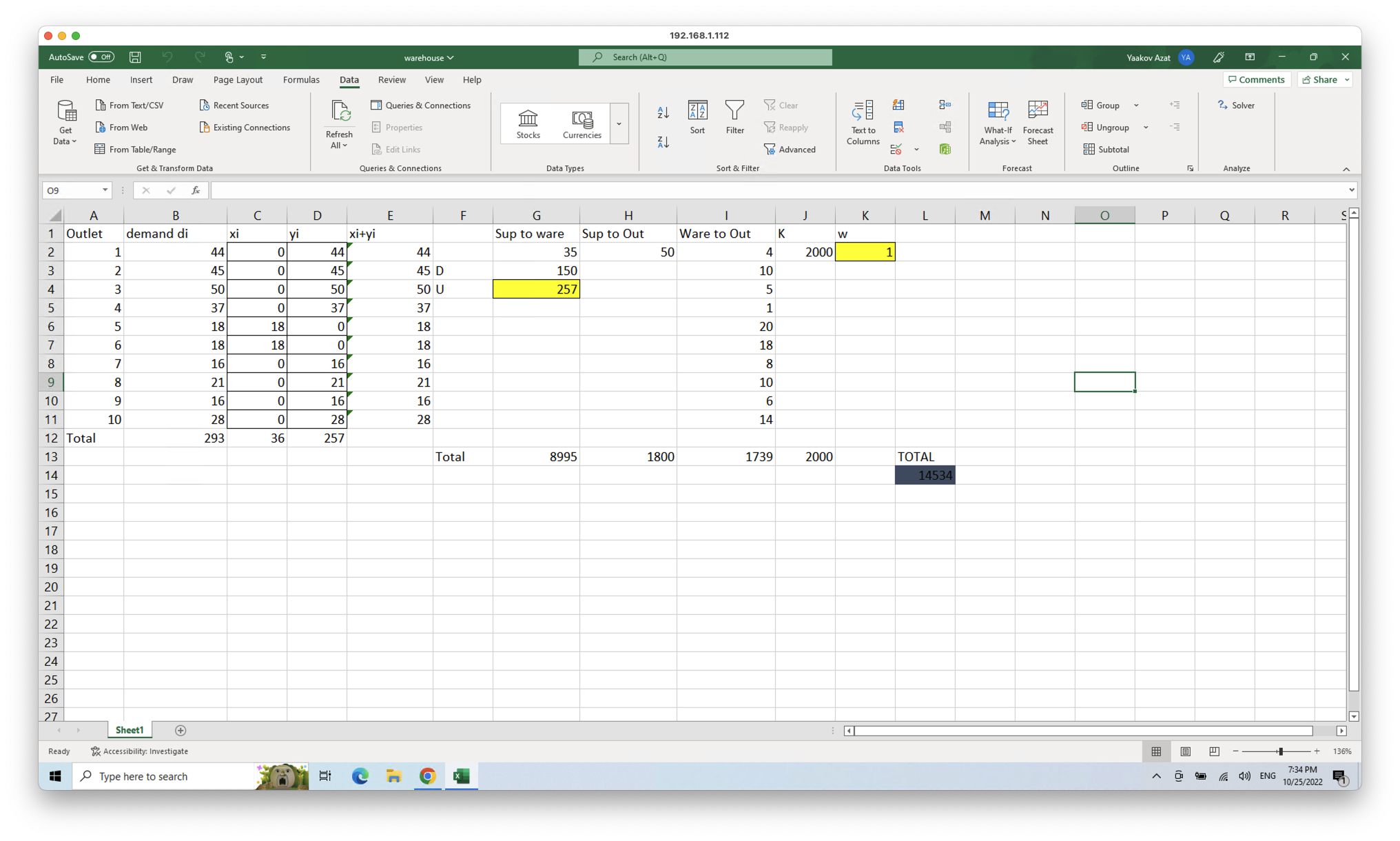

Solving with Excel Solver:

Update: 2022-10-24

[In detail explanation] (https://raw.githubusercontent.com/azataiot/images/master/2022/10/upgit_20221025_1666709901.pdf)

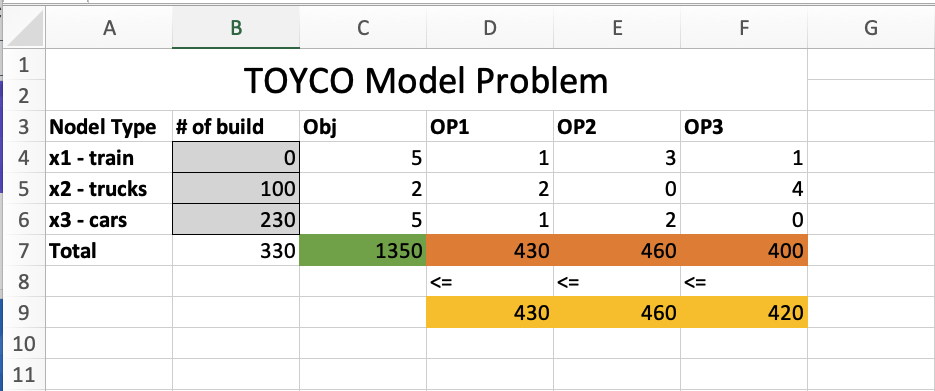

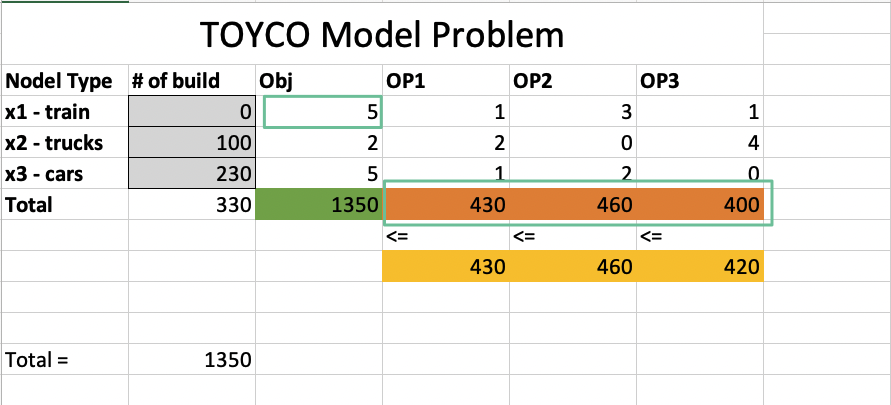

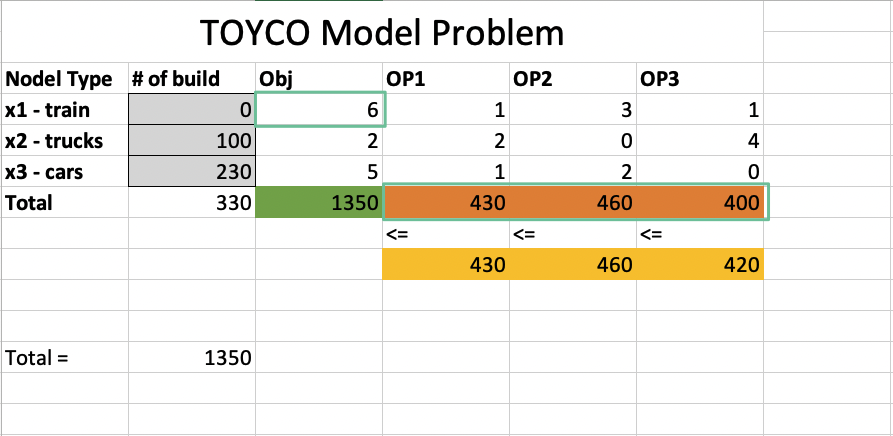

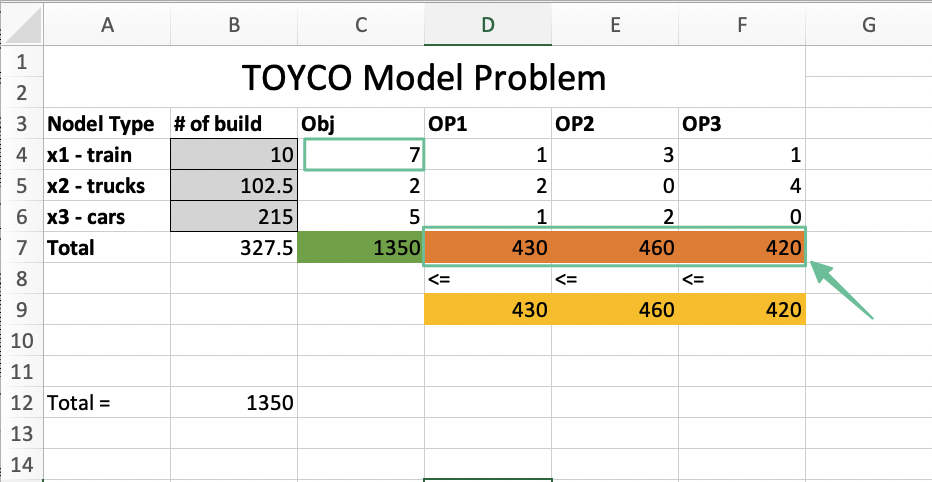

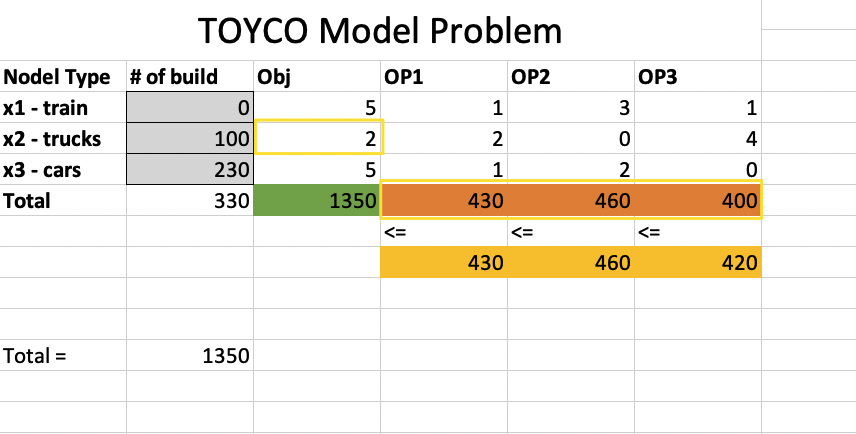

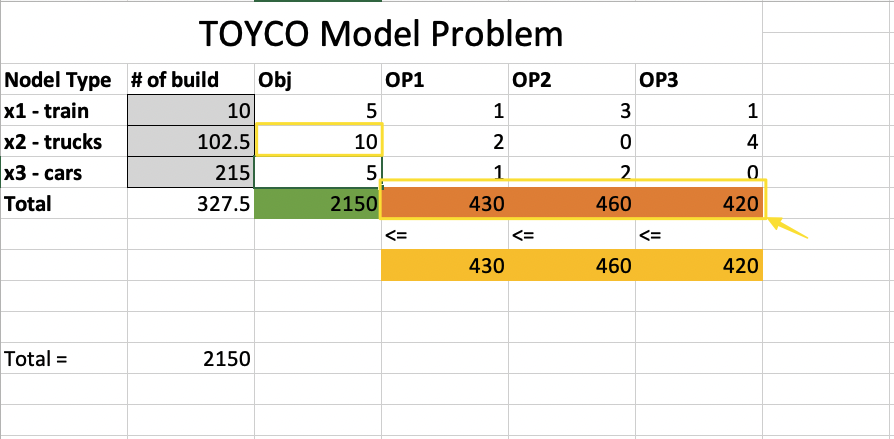

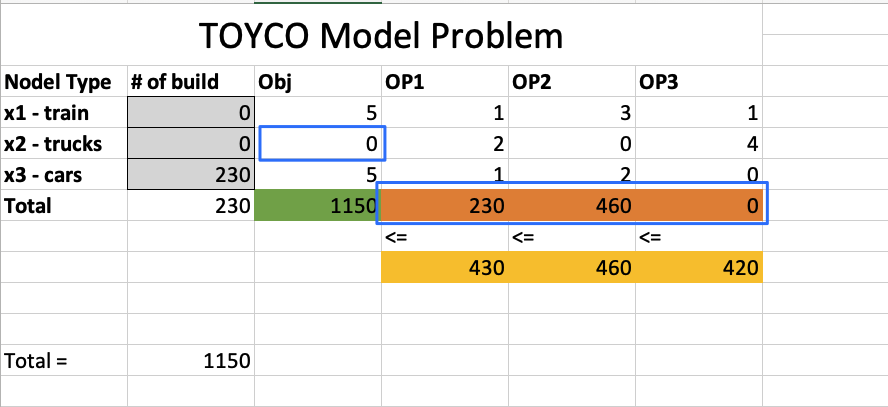

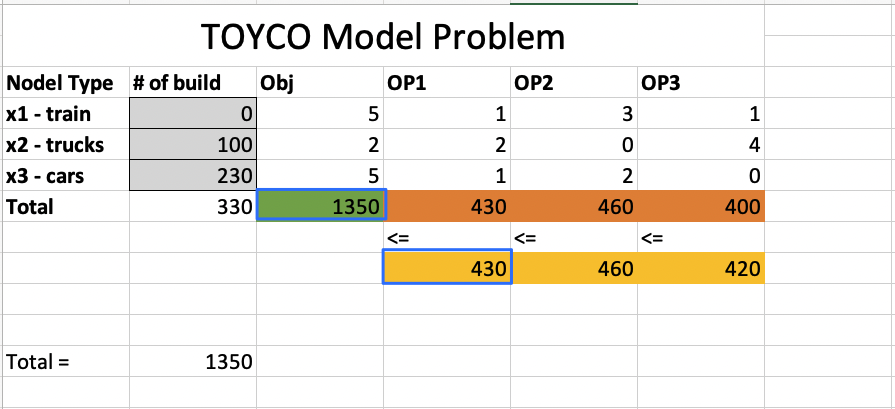

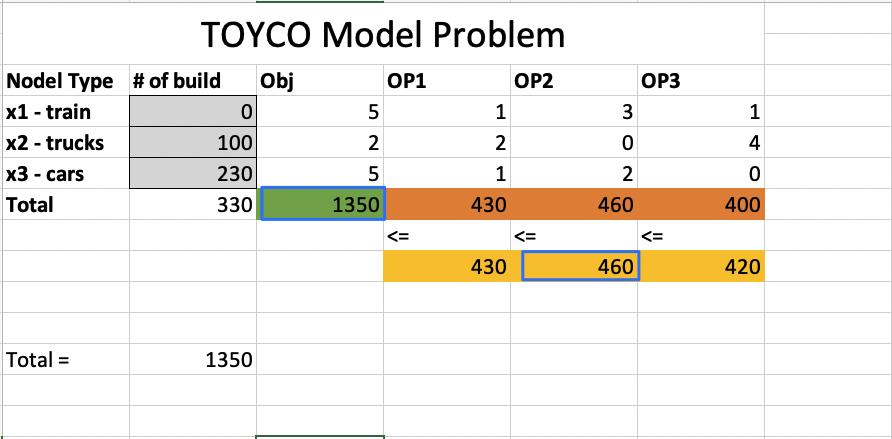

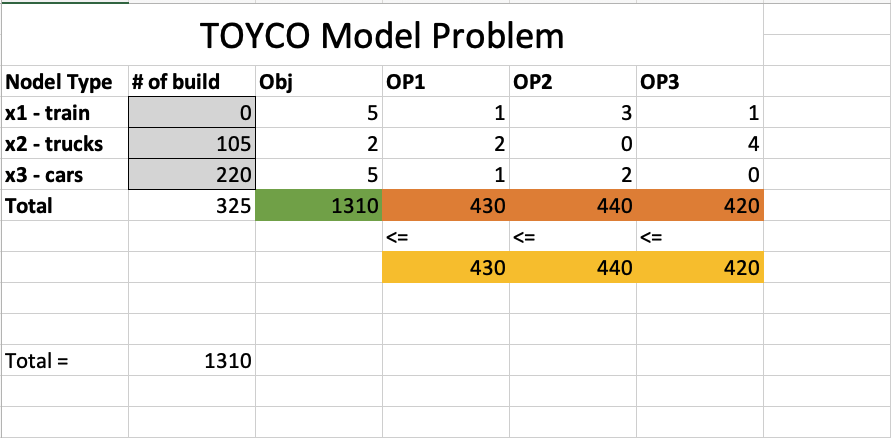

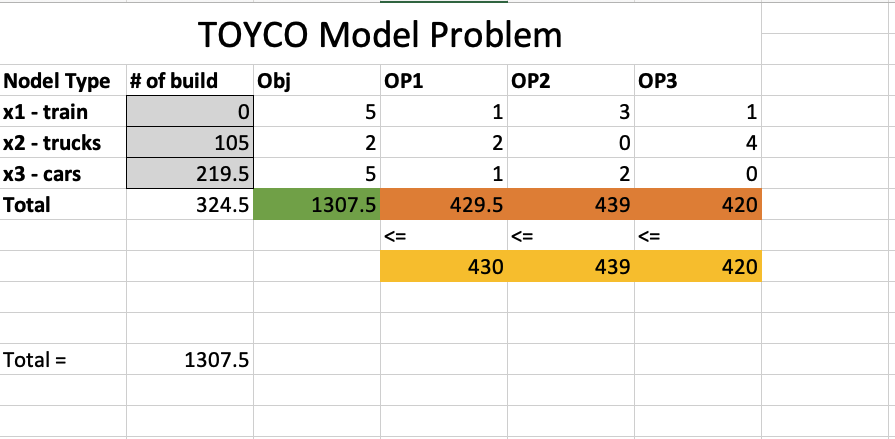

TOYCO Model

Decision variables

objective function

Constraints

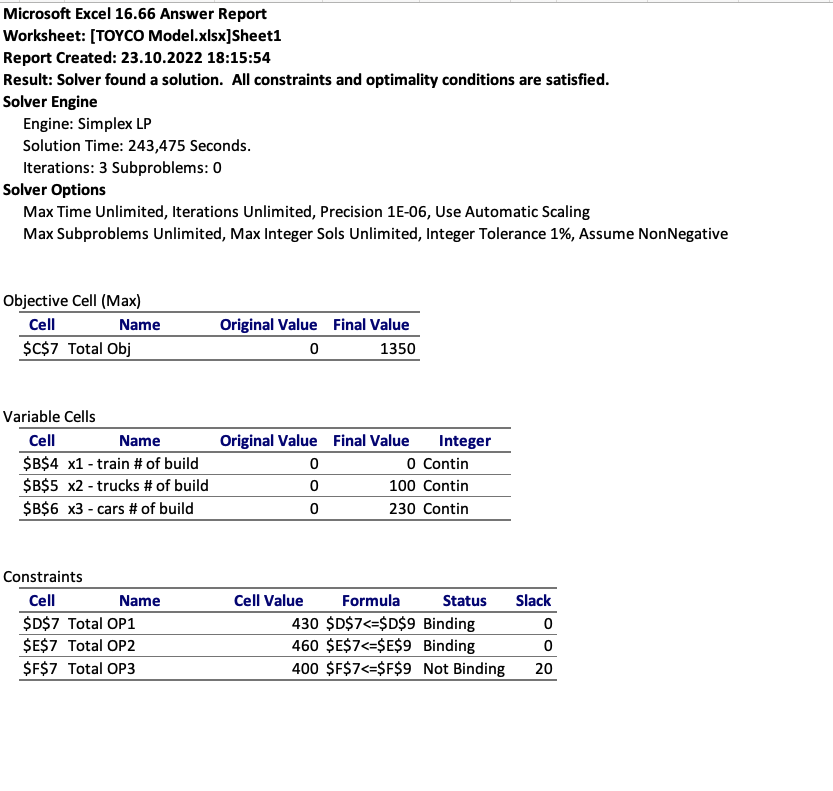

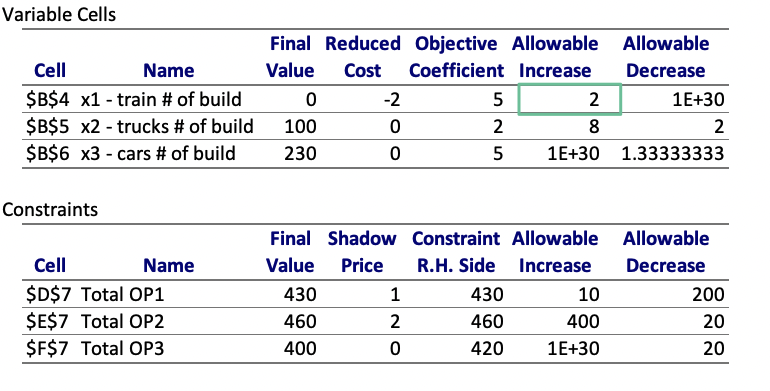

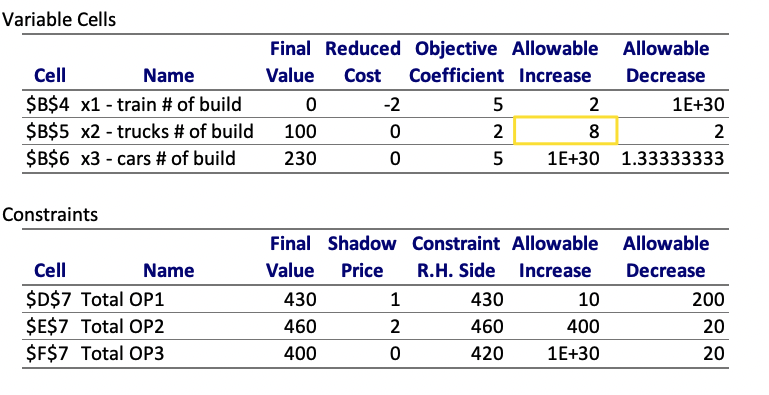

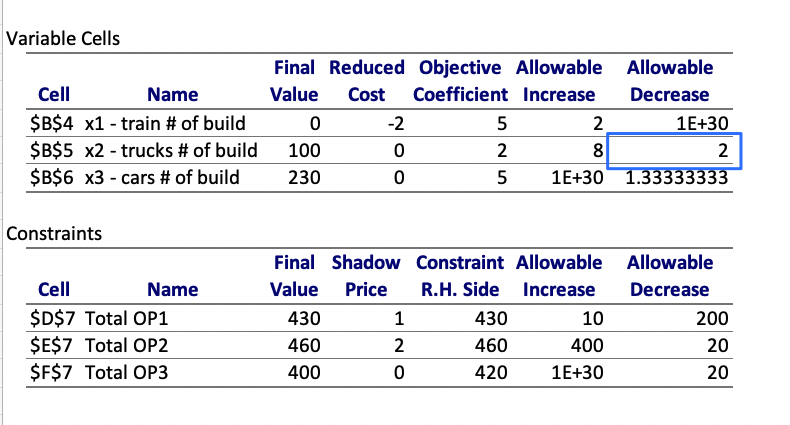

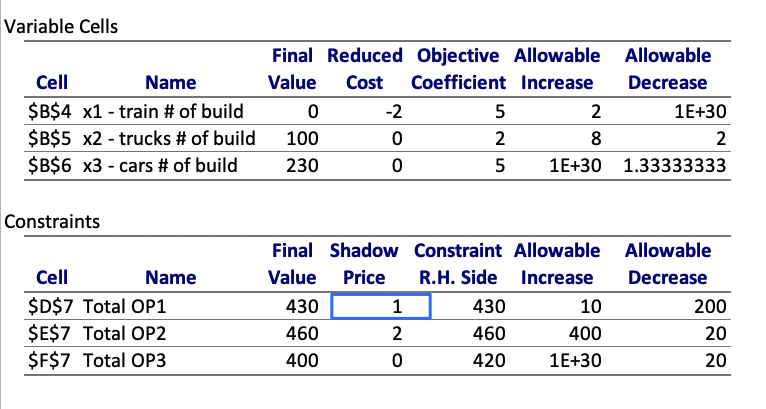

Answer Report

Notice Constraints - Total OP3 row, status is Not Binding, because we have slack of 20.

Slack is what you need to add to the LHS so that to make the inequality equal.

s : slack

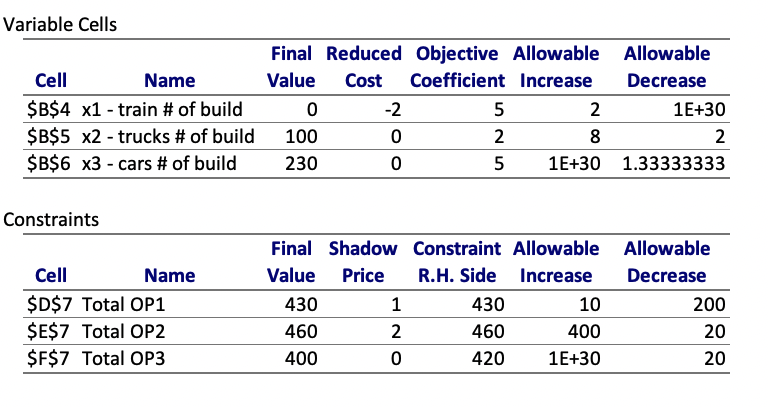

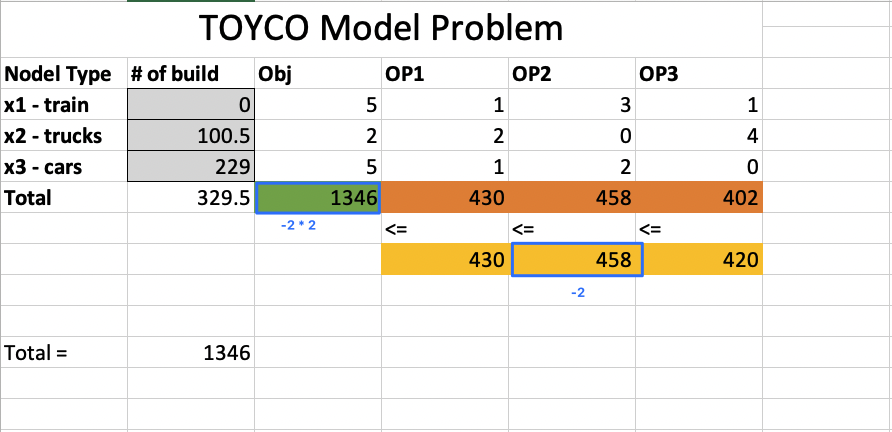

Sensitivity Report

In a linear program as

Final Value

Final values are the values ofx for the optimal z.

Reduced cost

The reduced cost for a variable is nonzero only when the variable’s value is equal to its upper or lower bound at the optimal solution.

The reduced cost measures the change in the objective function’s value per unit increase in the variable’s value.

The reduced costs tell us how much the objective coefficients (unit profits) can be increased or decreased before the optimal solution changes.

Allowable increase

Allowable decrease

Shadow Price

The Shadow Price for a constraint is nonzero only when the constraint is equal to its bound. ( all material used)

The Shadow Price measures the change in the objective function’s value per unit increase in the constraint’s bound.

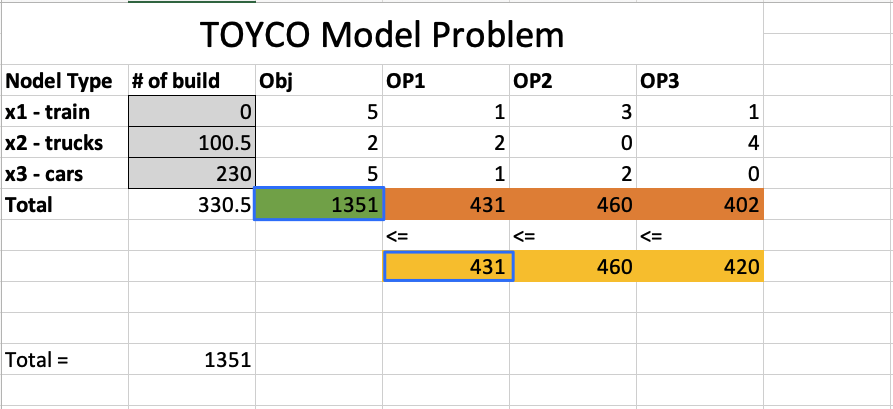

Allowable increase

The Allowable Increase and Allowable Decrease fields in the report show the range of increases and decreases for which the Reduced Costs and Shadow Prices remain constant.

Standard form of LPS

The standard form of an LPS is

Surplus and Slack value

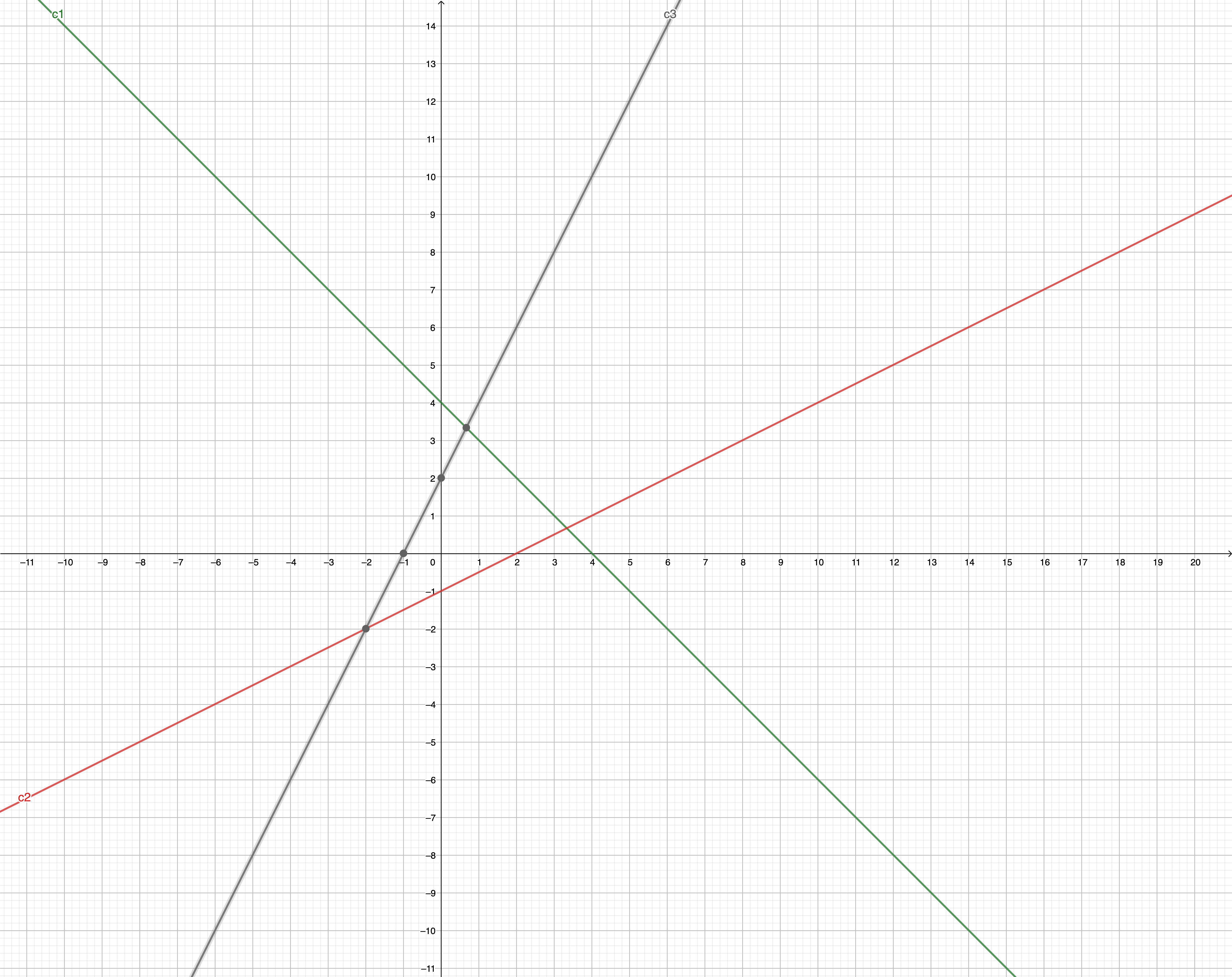

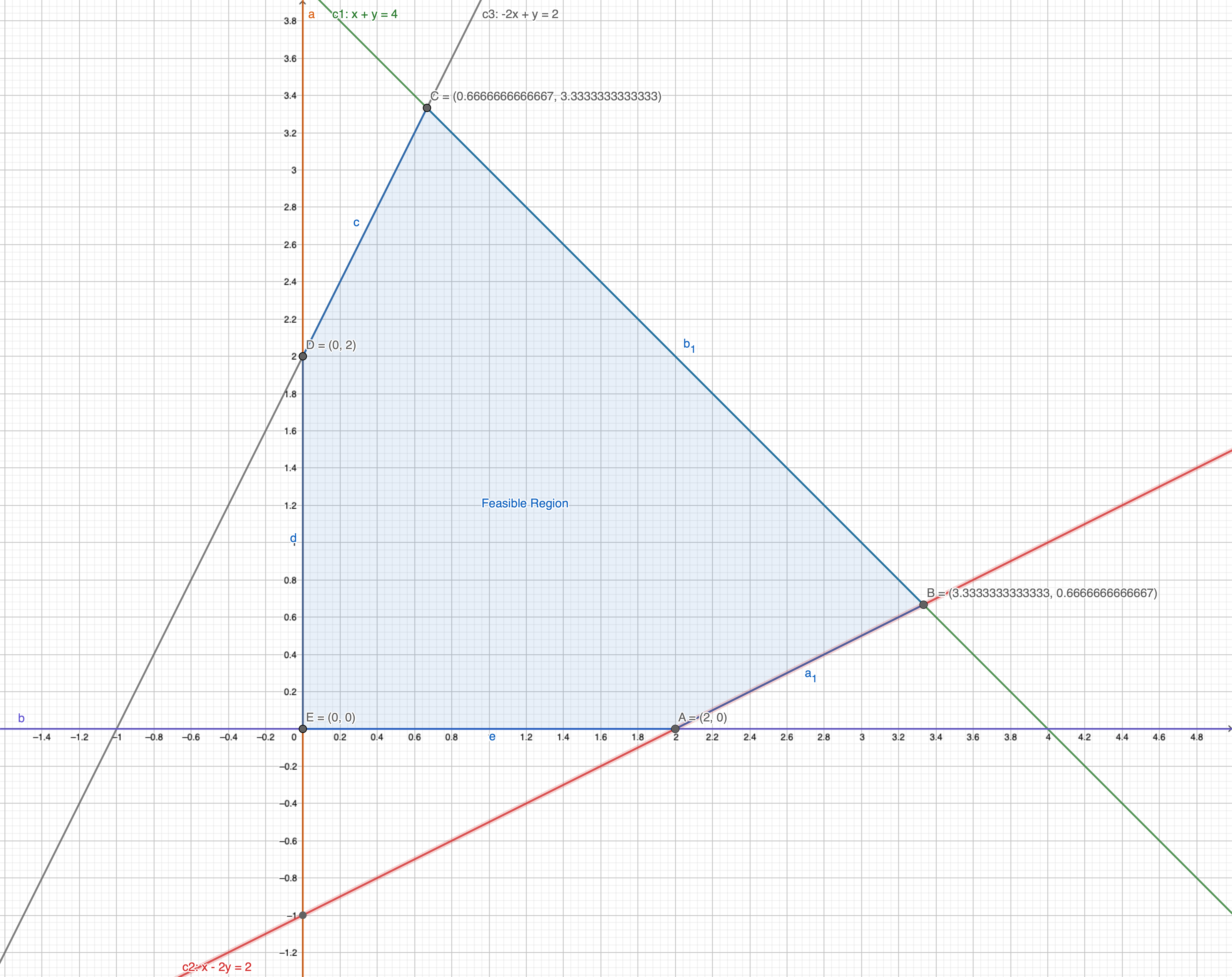

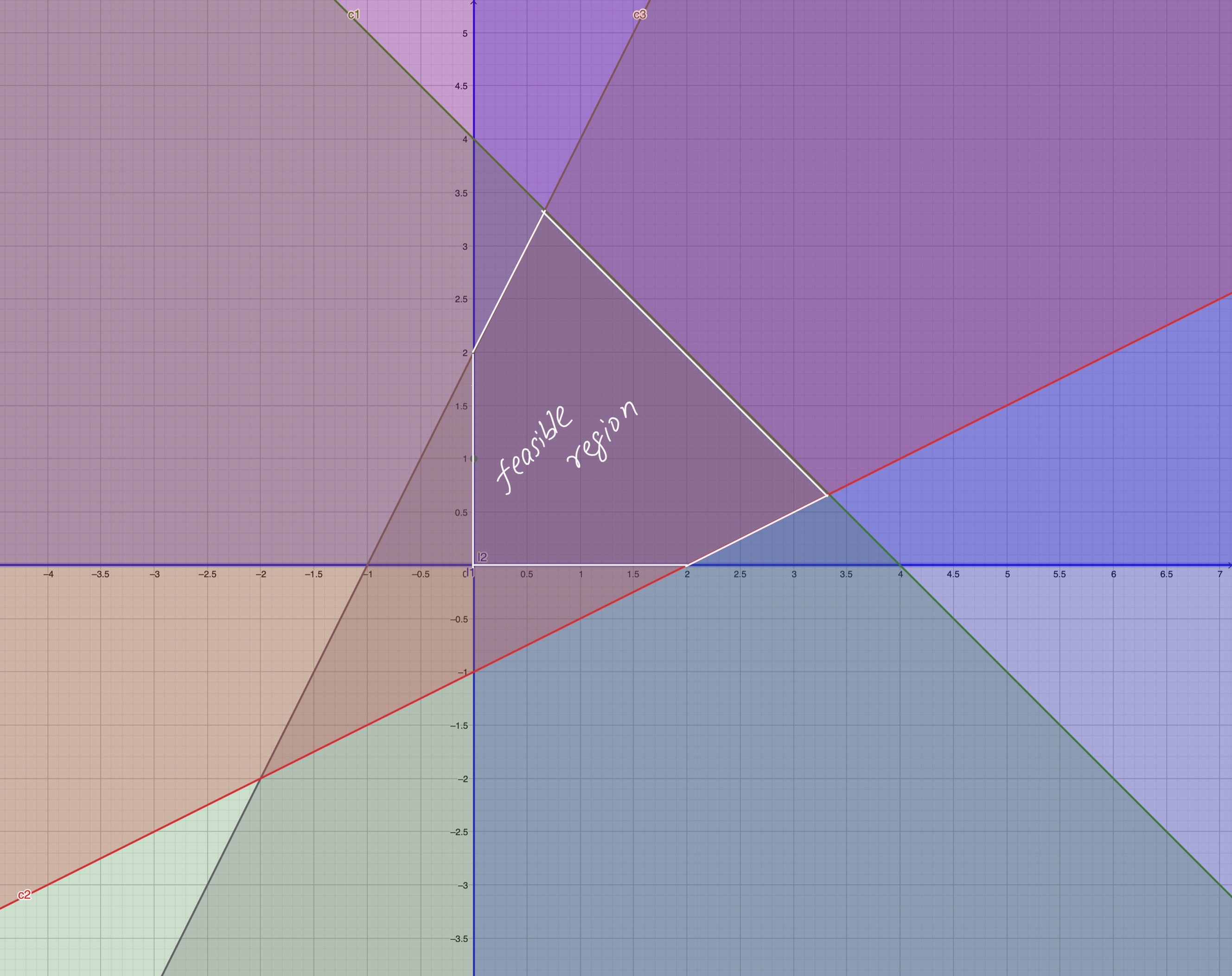

Graphical solution Procedure

First draw the

Then draw

Then

Then

Extras

Stanford cvx

Standofrd Convex Optimization Book